S&P 500 FUNDAMENTALFORECAST: BEARISH

- Volatility may be elevated in view of presidential debates and a pending US fiscal stimulus plan

- US presidential election, coronavirus resurgence, and rising US Dollar[1] are among the key risks

- Recent selloff may prove to be another “healthy correction” in the medium-term bull run

S&P 500 Index Outlook:

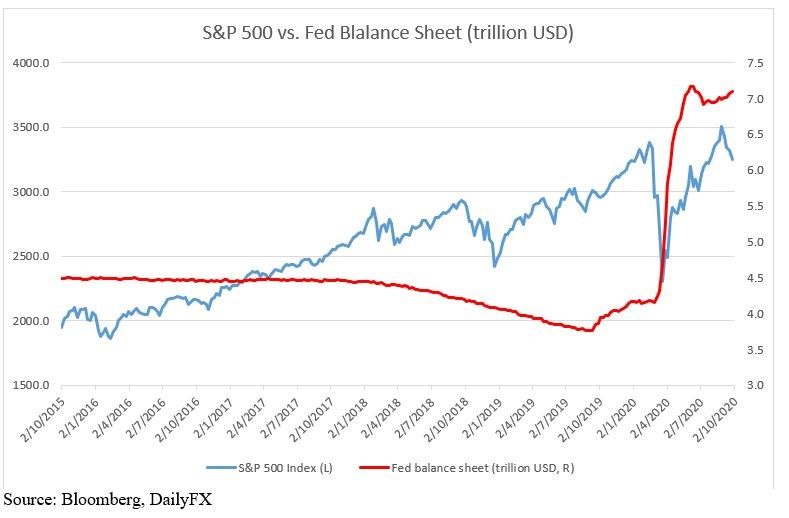

Since early September, US stock markets entered a consolidative phase, pausing a five-month rally that was mainly driven by recovery hopes and Fed’s balance sheet expansion. With the Fed members warning a lengthy recovery and lacking fiscal stimulus support, equity markets seem to have lost some steam. Unwinding activities were seen in risk assets, whereas safe-haven assets were on bid. The US Dollar Index (DXY) has climbed to a two-month high of 94.4.

Although the central bank has signalled no rate hikes until year 2023 in the latest FOMC[2] meeting, a slowdown in the Fed’s balance sheet expansion and its reluctancy to ease more weighed on market sentiment (chart below).

S&P 500 Index vs. Fed Balance Sheet (2015-2020)

Some near-term headwinds include the US presidential election, a ‘second wave’ of coronavirus in parts of the EU, and a pending US fiscal stimulus package. The first Trump – Biden presidential debate will be held next week, September 29 from 9:00-10:00 P.M. ET. This debate may draw millions of viewers and market volatility may rise during the debate. The CBOT VIX term structure has likely priced-in higher volatility associated with options on the S&P 500[3] index leading up to the November election (chart below).

Besides, credit risks are soaring among China’s property developers, most of which are highly leveraged. Evergrande, one of China’s largest real estate company, has warned of a possible debt restructuring if