DOW JONES, NASDAQ 100, S&P 500 FUNDAMENTALFORECAST: BULLISH

- Q4 US corporate earnings may surprise markets to the upside with more upward EPS revisions

- Financials, materials and communication services sectors saw largest jump in earnings forecasts

- The S&P 500[1] index price-to-earnings (P/E) ratio is now above 30.0, well over its 5-year average

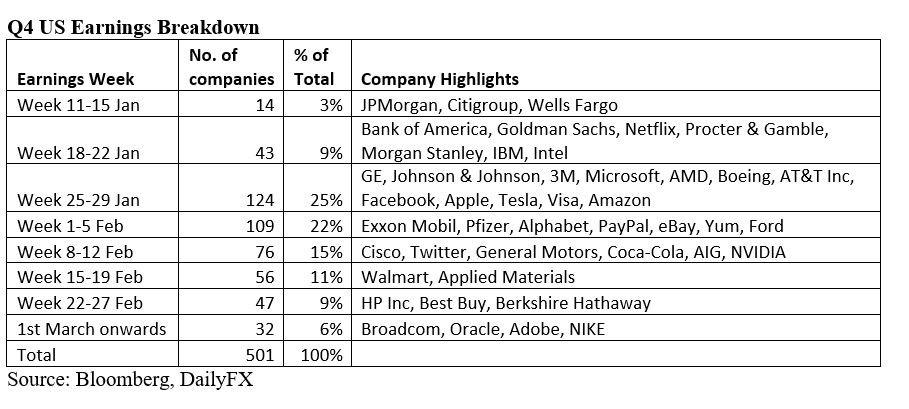

The Q4 earnings season is around the corner, with about 9% of the S&P 500 companies reporting their results in the week of 18-22 January. Peak earnings season arrives in the last two weeks of January 2021, with 25% and 22% of the S&P 500 components releasing results respectively (table below). By then, major American banks and the five FAANG stocks (Facebook, Apple, Amazon, Netflix and Google) would have delivered their scores, which are critical to the performance of the S&P 500, Dow Jones[2] and Nasdaq[3] 100 indices. Investors will focus on fundamental metrics and assess how Corporate America fared in the winter when another severe viral wave hit the economy.

Analysts and companies were increasingly optimistic about Q4 earnings, with the estimated EPS decline for the quarter revised up to -8.8% from -12.7% seen in the end of September, according to data compiled by FactSet. Only 29 S&P 500 companies have issued negative EPS guidance, compared to 56 that gave a positive assessment. Among companies with negative Q4 EPS estimations, the majority are in the aviation, entertainment, tourism, hospitality and energy sectors that were hit the hardest by Covid-related restrictions.

Sector-wise, the largest upward earnings revisions were observed in the financials sector (from -24.1% to -7.5%), led by big banks such as JP Morgan, Bank of America, Citigroup and Goldman Sachs. The outlook for the materials (from -2.0% to 7.1%) and communicationservices (from -18.2%