Implied volatility, synonymous with expected volatility, is a variable that shows the degree of movement expected for a given market or security. Often labeled as IV for short, implied volatility quantifies the anticipated magnitude, or size, of a move in an underlying asset.

WHAT IS IMPLIED VOLATILITY?

Implied volatility is a number displayed in percentage terms reflecting the level of uncertainty, or risk, perceived by traders. IV readings, which are derived from the Black-Scholes options pricing model, can indicate the degree of variation expected for a particular equity index, stock, commodity, or major currency pair[1] over a stated period of time.

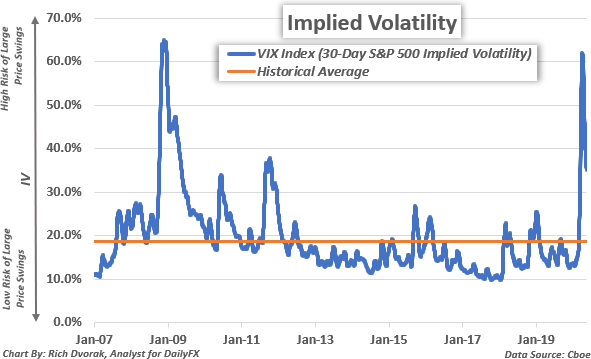

For instance, the popular VIX Index is simply the 30-day implied volatility reading for the S&P 500[2]. A high VIX level (i.e. percent), or high implied volatility reading, indicates that risk is relatively elevated and there is a greater chance of larger than normal price swings.

IMPLIED VOLATILITY VS HISTORICAL VOLATILITY – WHAT IS THE DIFFERENCE?

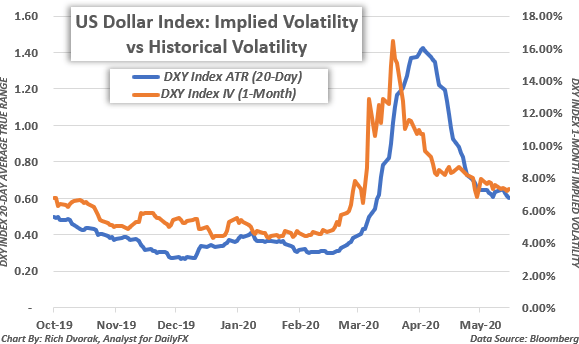

Implied volatility is the expected size of a future price change. Implied volatility broadly reflects how big or small of a move is anticipated to be over a particular time frame. On the other hand, historical volatility[3], or realized volatility, indicates the actual size of a previous price change. Historical volatility illustrates the overall level of market activity that has already been observed.

The average true range (ATR[4]) of an asset or security is an example of an indicator that illustrates historical volatility. Though implied volatility and historical volatility differ slightly in the regard of future expectations versus past observations, the two metrics are closely related and tend to move in similar patterns.

Implied volatility readings are typically higher when there is a large degree