Japanese Yen, USD/JPY, Fed, Inflation, Inelastic Travel Demand – Third Quarter Fundamental Forecast

- Japanese Yen[1] weakness slowed in the second quarter, road ahead not easy

- A key upside factor for USD/JPY[2] remains a less-dovish Federal Reserve

- Inelastic travel demand, vaccination rates may keep US inflation elevated

To read the full Japanese Yen forecast, including the technical outlook, download our new 3Q trading guide from the DailyFX Free Trading Guides!

Japanese Yen Second Quarter Recap – Dominant Downtrend Slows

As expected from the second-quarter fundamental outlook, the Japanese Yen spent most of its time weakening against its major counterparts before the third quarter. Albeit, its pace of deprecation notably slowed compared to what occurred in the first quarter. The anti-risk currency is likely not receiving much attention due to a persistent decline in stock market volatility.

While there have been some moments of brief volatility when looking at global sentiment, a lasting trend was notably absent. A revival in volatility remains a prominent upside potential for the Yen, but ongoing loose monetary policy around the world could keep market sentiment from materially souring. Rather, the Yen will likely remain glued to developments in government bond yields.

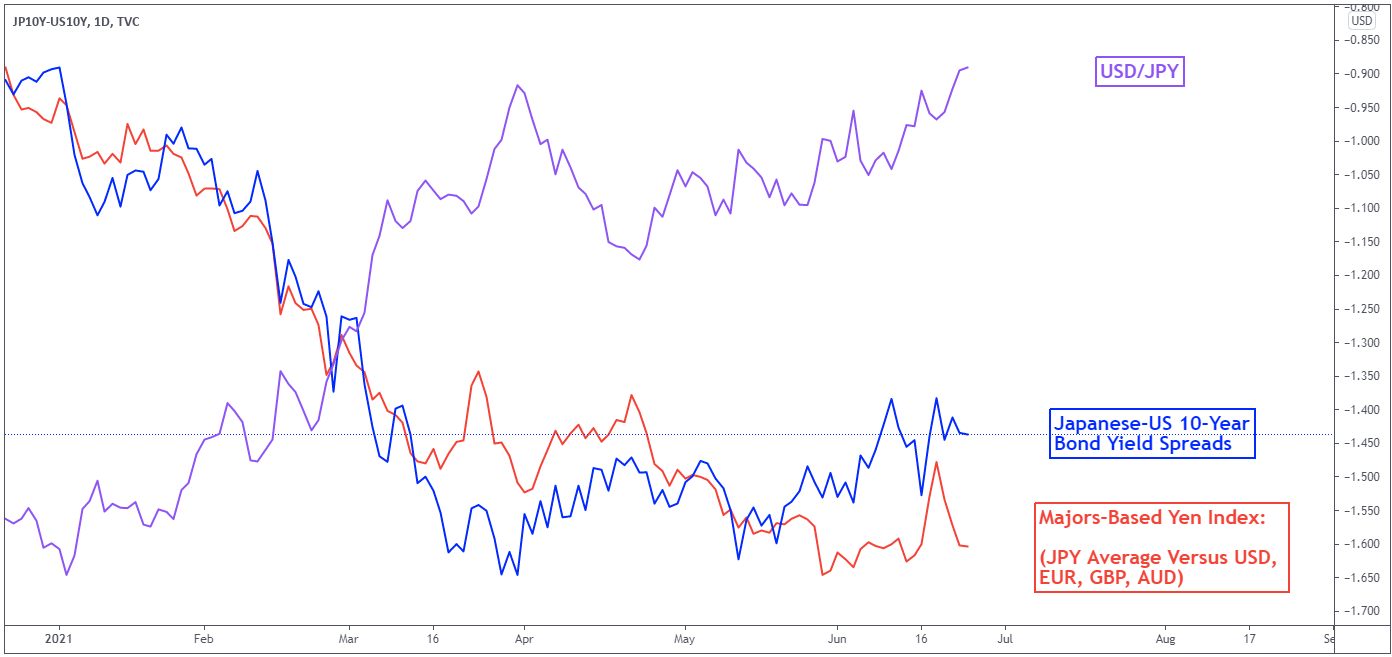

Majors-Based Japanese Yen Index Versus Bond Yields and USD/JPY

Chart Created in TradingView[3]

The Tough Road Ahead for the Yen

In the chart above, my majors-based Yen index can be seen somewhat closely following spreads between Japanese and United States 10-year government bond yields. During the second quarter, Japanese bond rates made a slight comeback against their US counterparts. This is as the Federal Reserve repeatedly reiterated its dovish stance, cooling concerns about sooner-than-expected tapering.

But, June’s Fed rate decision showed that more members are starting to see a rate hike as appearing nearer on the horizon. This also