Rand Fundamental Backdrop

The rand has displayed robust defiance throughout Q2 despite persistent local economic and political woes. This is no surprise as throughout the COVID-19 pandemic, the ZAR has predominantly been driven by external global factors. Risk sentiment has played a continual role in dictating rand trends along with its Emerging Market (EM) currency counterparts.

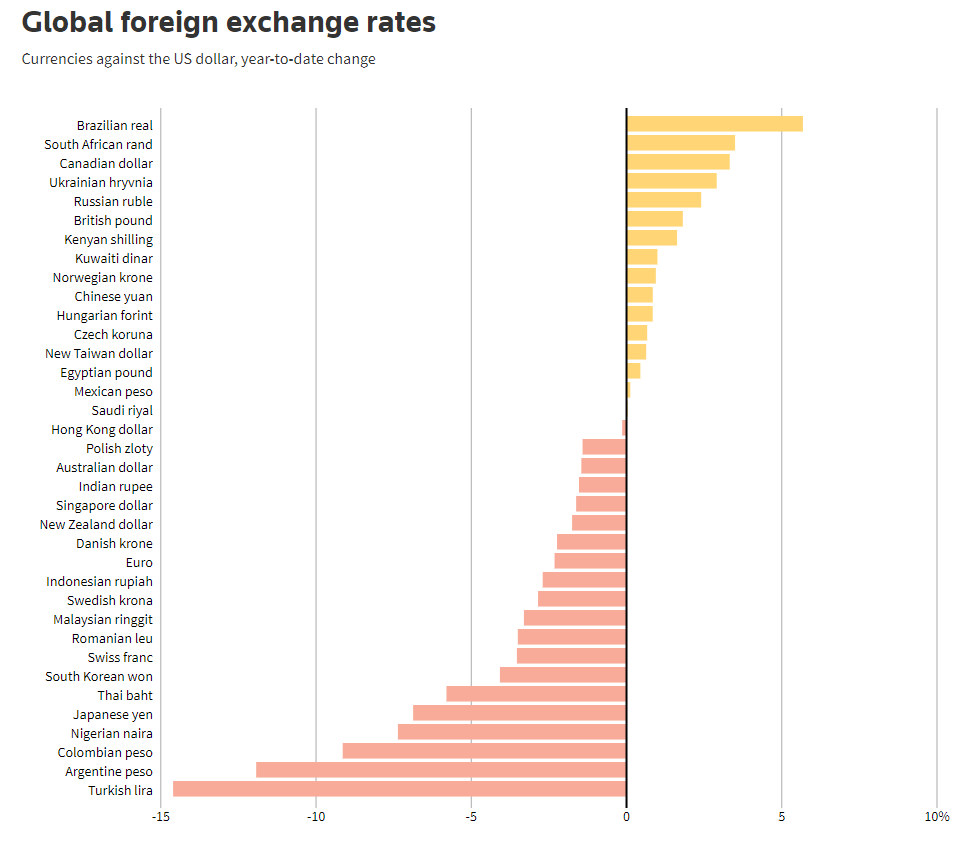

Other EM currencies have also performed strongly but the rand has held the top spot against the dollar for most of 2021 with the Brazilian Real recently taking over.

The reasoning behind this outperformance has not been down to rand strength but rather comparatively worse conditions experienced in peer nations. For example, India with their escalating COVID-19 condition, while Russia and Turkey’s geopolitical risks carry resistance for their respective currencies.

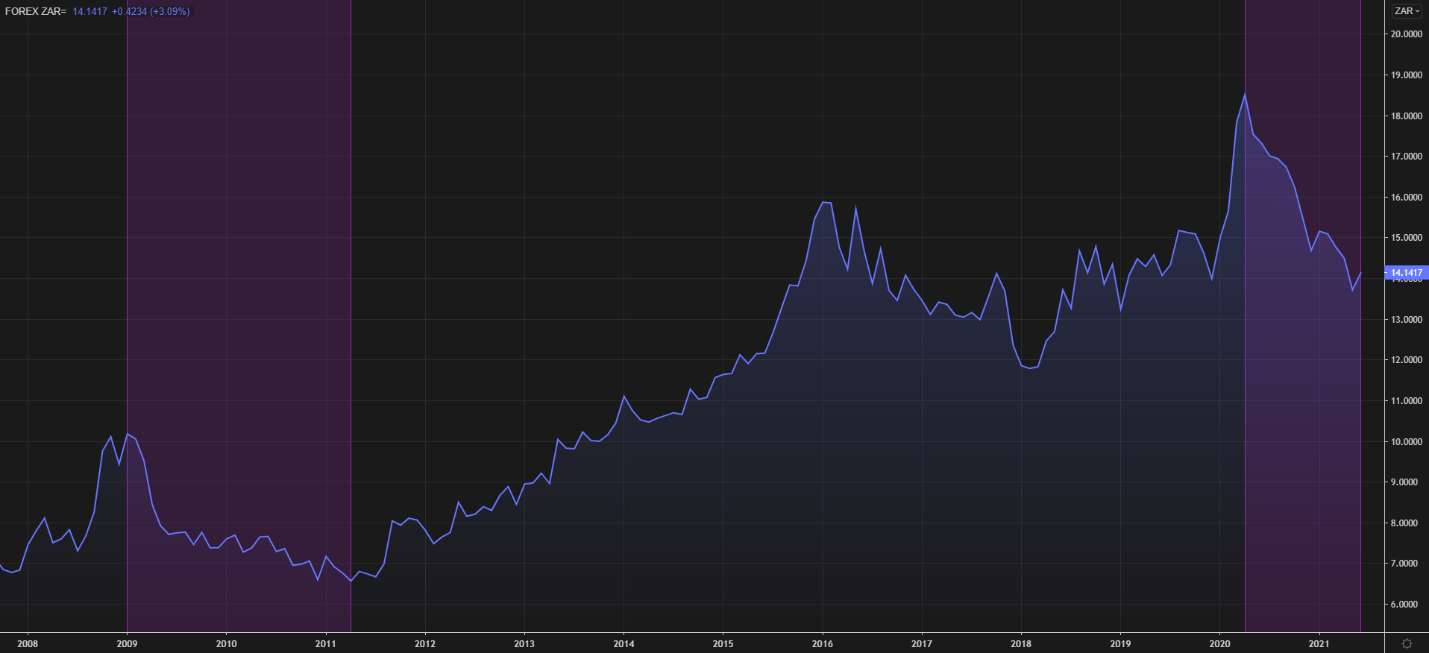

USD/ZAR Financial Crisis Vs Covid-19

Chart prepared by Warren Venketas, Refinitiv

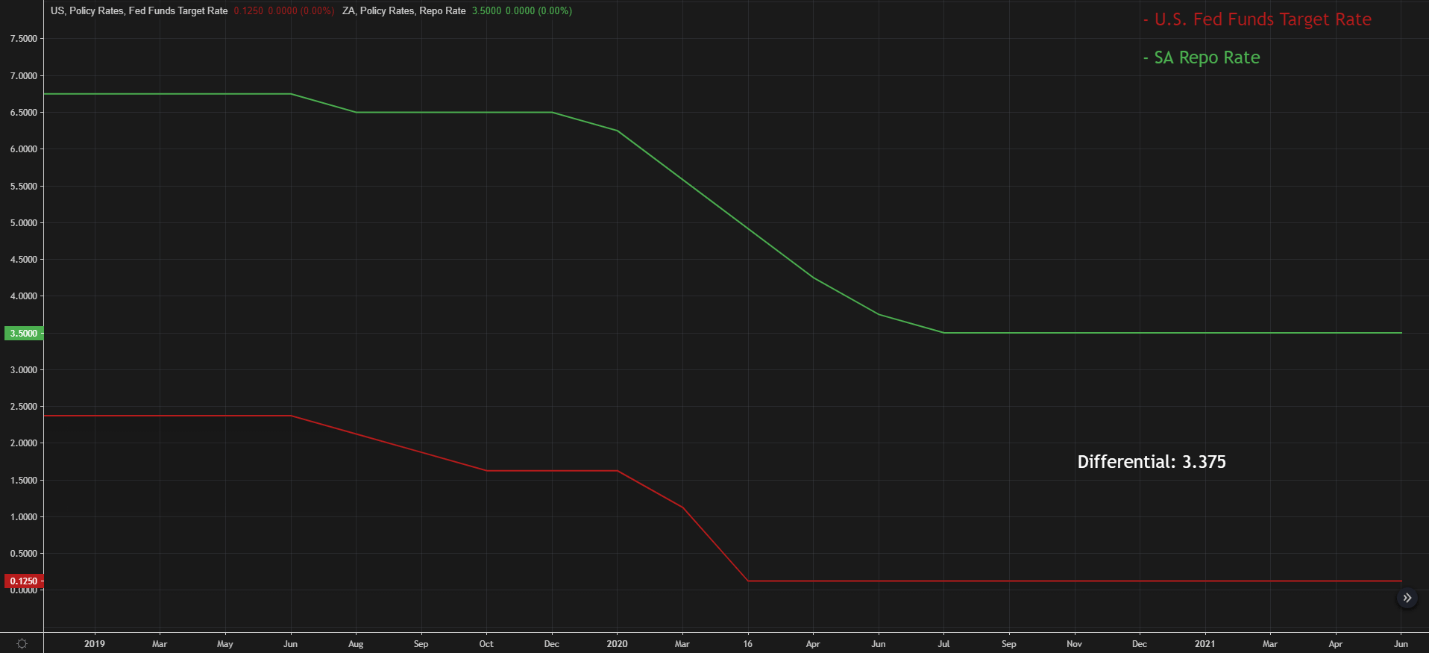

The carry trade element remains in place in Q3 as the U.S. Federal Reserve continues with low interest rates - even though longer-term interest rate hikes have been brought forward after the Q2 FOMC[1] meeting in late June. An interesting comparison between the financial crisis in 2007/8 and the current COVID-19 pandemic (see chart above) shows a similar trend in the way of noteworthy rand strength against the dollar post-rate cuts (purple).

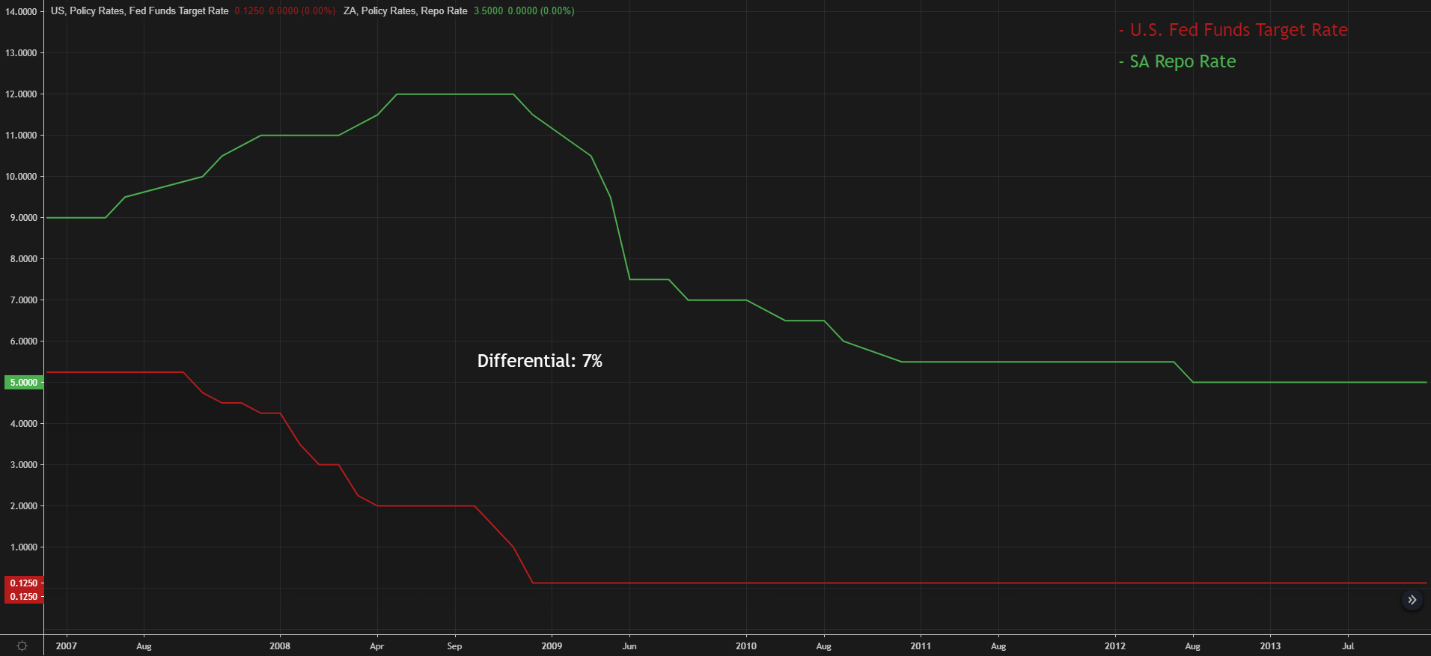

Fed Funds Rate Vs SA Repo Rate: 2007 - 2013 (Financial Crisis)

Fed Funds Rate Vs SA Repo Rate: 2019 – Present (Covid-19 pandemic)

USD/ZAR[2] fell roughly 45% from the October 2008 high to the May 2011 low. While current levels on USD[3]/ZAR show a decline of approximately 30% off April 2020 highs. Does this mean the situation is like-for-like? In a nutshell, no. I do not believe USD/ZAR will fall a further 15% in this case as the