Dow Jones, S&P 500, Nasdaq 100 Talking Points:

- Seasonality may drag on price action as the summer doldrums weigh on market activity

- Tight trading ranges are not inherently bearish, however, and the broader fundamental landscape remains encouraging

The Dow Jones[1], S&P 500[2] and Nasdaq[3] 100 entered the third quarter on the back of yet another strong showing in the post-pandemic era as stocks continued to climb across all sectors. With the broader economic recovery set to provide a modest tailwind for the major indices, equity investors will have to negotiate seasonality concerns, monetary policy changes and infrastructure spending as they attempt to nail down the finer details driving stock valuations in the coming quarter.

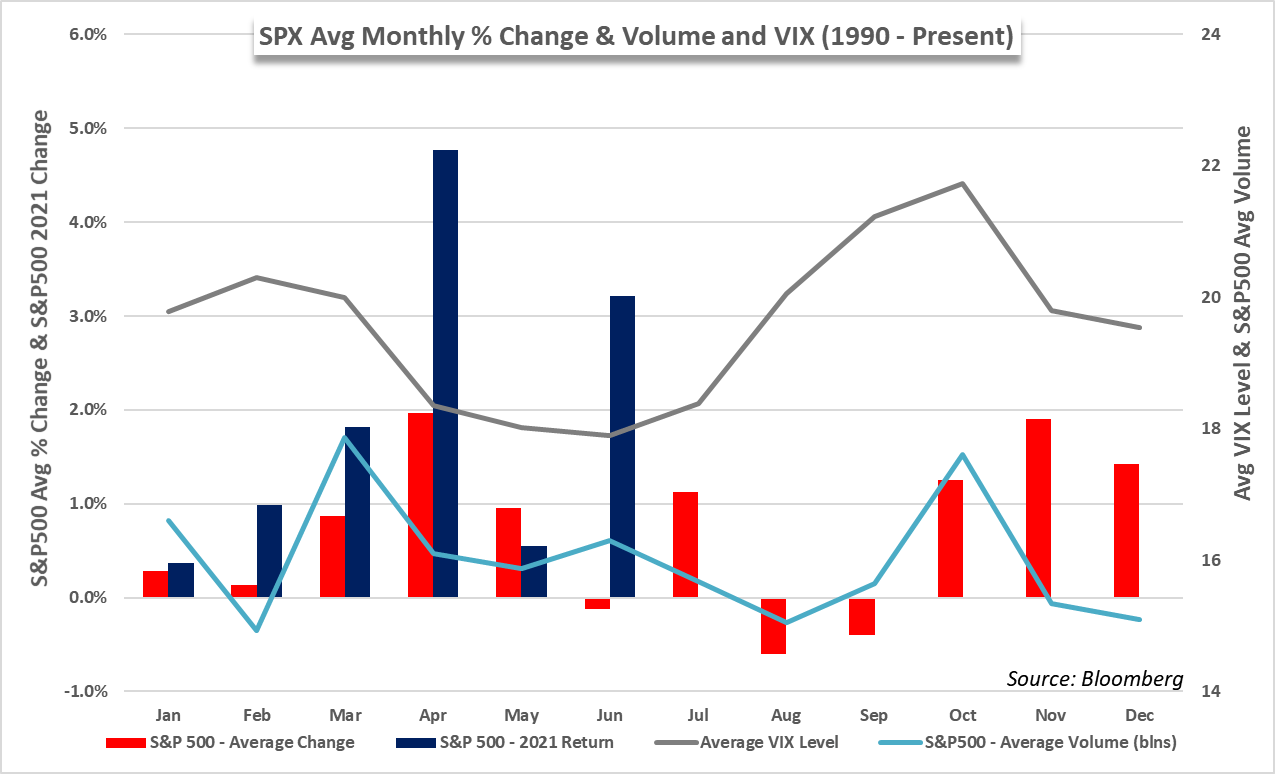

While the general equity landscape is largely conducive to further gains, seasonal headwinds may look to constrict price action and slow attempts higher. Since 1990, the S&P 500 has seen some of its lowest trading volume in July, August and September; and if the tail end of the second quarter was any indication, price action may dry up across markets without a new set of catalysts.

Chart 1: S&P 500 Average Monthly Returns & Average Monthly VIX

Source: Bloomberg

Lower volume and volatility are not exclusively bearish factors by any means, but they can make it more difficult for price breakouts to occur and for follow-through to take place if a breakout does materialize. To read the full Equity forecast including the technical outlook, download our new 3Q trading guide from the DailyFX Free Trading Guides!

DailyFX[4] provides forex news and technical analysis on the trends that influence the global currency markets.