Markets experienced some turbulence last week as freefalling bond yields concerned investors and fueled an unwind of the reflation trade. The ten-year Treasury yield, for example, plunged as much as 20-basis points to a low of 1.25%. This corresponded with a sharp pullback in risk appetite that sent the Dow Jones[1] spiraling -1.8% lower mid-week.

Crude oil prices[2] similarly came under pressure with the commodity sinking -5.9% at its weekly low. Fear surrounding the delta covid variant – and its potential to weigh negatively on global growth prospects – stood out as one key driver of the move. Nevertheless, trader sentiment improved considerably later in the week with the Dow, S&P 500[3], and Nasdaq[4] all closing at record highs on Friday. That appeared to follow NIAID Director Dr. Fauci announcing how FDA-approved covid vaccines are effective against the delta variant.

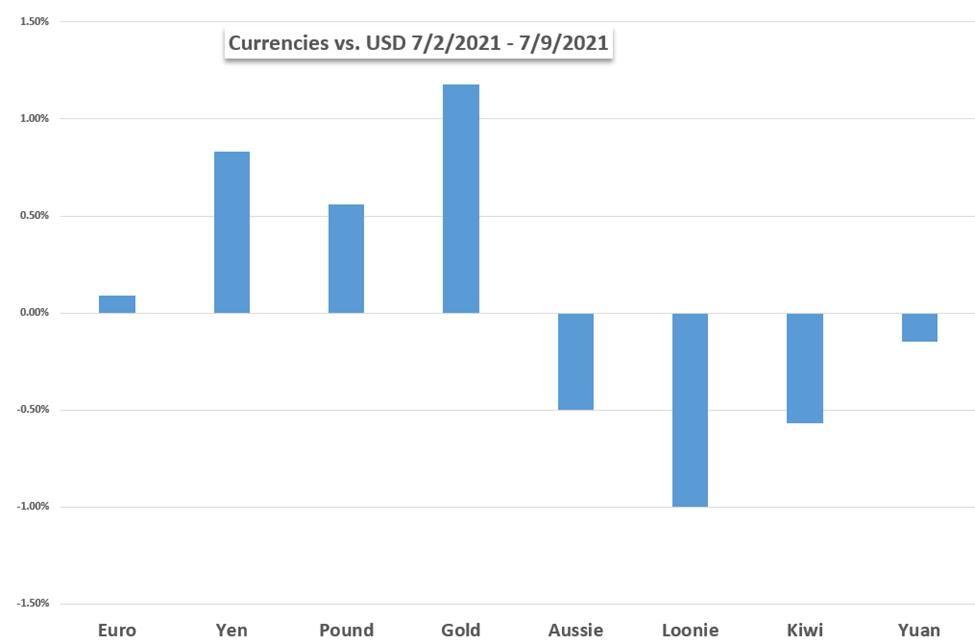

Gold[5] gained 1.5% to close above the $1,810-price level largely thanks to recent bond market volatility. The drop in sovereign interest rates helped drag USD/JPY[6] price action lower as lower real yields benefited the Japanese Yen[7] across the board of major FX peers. EUR/USD[8] whipsawed to finish 13-pips higher on balance after weakening to its lowest level since 05 April with Euro[9] bulls deterred little by the ECB shifting its inflation mandate to allow for overshoots of the symmetric 2% target.

MAJOR CURRENCIES AND GOLD PERFORAMCNE AGAINST US DOLLAR

Looking to the week ahead, markets will need to weather an economic calendar[10] jam-packed with high-impact event risk. The release of US inflation data will likely be front-and-center with the monthly CPI report due Tuesday, 13 July at 12:30