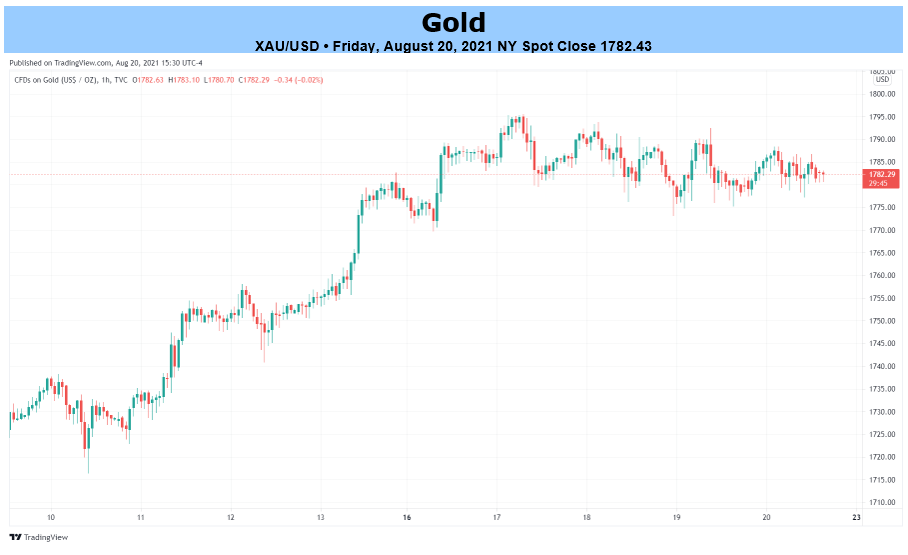

XAU/USD ANALYSIS

GOLD FUNDAMENTAL BACKDROP

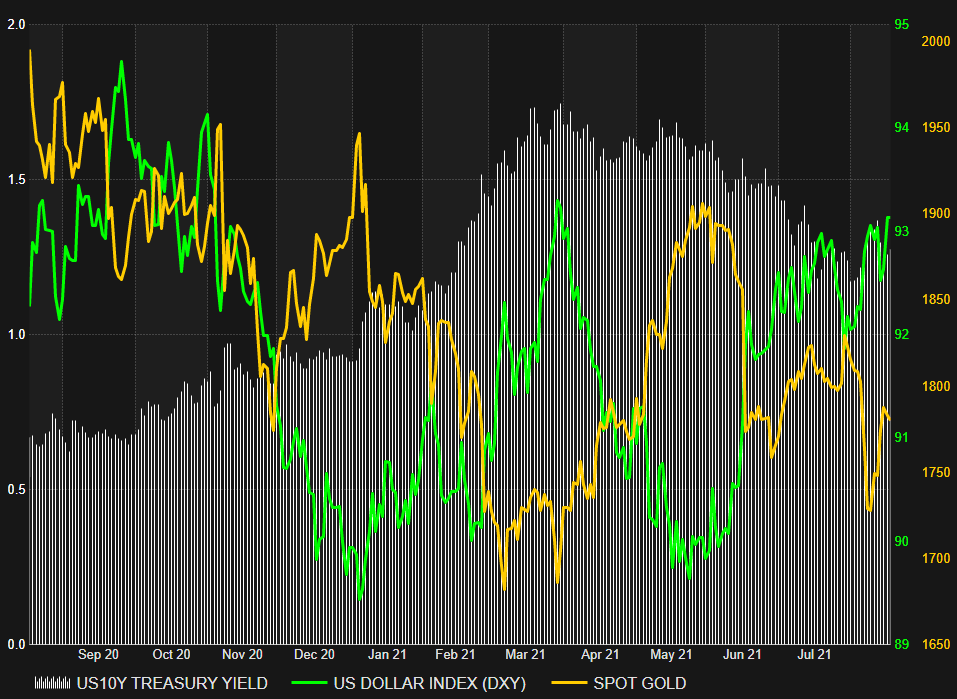

The historical inverse relationships between gold[2] and both the greenback and U.S. Treasury yields respectively are weighing in on the precious metal. The Dollar Index (DXY)[3] has held its high level of negative correlation to gold while bond yields have been displaying a change of heart since late April 2021 (note correlation does not mean causation!).

The chart below illustrates this phenomenon as seen by the green and white synchronicity towards the right hand side of the chart. It seems as if the dollar[4] is the main driver for gold prices between the two. The current low interest rate environment also accommodates higher gold prices but unfortunately for gold bulls, the prices do not reflect the underlying fundamentals at this moment.

Spot Gold vs U.S. 10-year Treasury yield vs DXY:

Source: Refinitiv Datastream

Fundamentally, we may see a rally in gold with the delta variant plaguing much of the developing world as well as many key financial and logistical hubs such as the recent China port shutdown as well as Australia and New Zealand’s ‘zero tolerance’ approach to COVID-19. The safe-haven[5] affinity with gold has been helping prices hold its head above key levels since the selloff two weeks prior.

The FOMC[6] minutes held last week Wednesday gave some guidance to market participants that QE tapering will resume before the end of 2021. In 2013, taper talk led to rising Treasury yields which hammered gold prices. The approach from the Fed[7] has been more cautious this time around with markets relatively unresponsive to last week’s meeting.

Many people