US Dollar Fundamental Forecast: Neutral

- USD[1] sank after non-farm payrolls report miss sapped Fed tapering bets

- Domestic economic docket fairly light ahead, placing focus on other news

- Key external event risk include the RBA, ECB and BoC rate[2] decisions

US Dollar Reaction to Non-Farm Payrolls Data, Key Implications

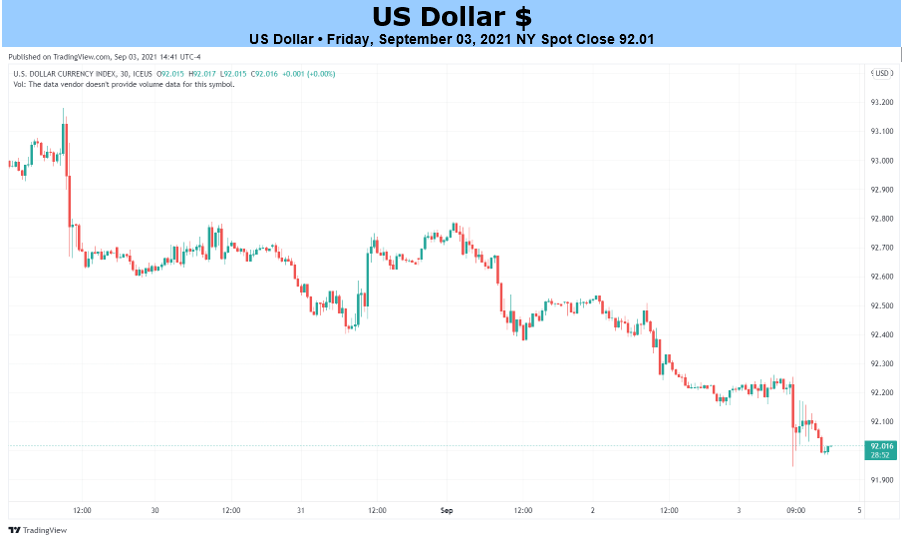

The US Dollar[3] weakened after Friday’s non-farm payrolls report largely missed expectations[4]. This sent my majors-based USD index to its lowest since July levels on the chart below, leaving behind 2 weeks of disappointing price action. The nation added just 235k jobs versus 733k anticipated as the unemployment rate declined to 5.2% from 5.4% - as anticipated. Average hourly earnings did surprise higher though at 4.3% y/y.

With that in mind, this report likely cooled expectations that the Fed could begin tapering monetary policy this month. This follows dovish commentary from Chair Jerome Powell on the labor market[5]. Moreover, further soft employment readings could delay eventual rate hikes in the long run. This is perhaps why the longer-term 10-year Treasury yield gained in the aftermath of the jobs report.

External Event Risk: RBA, ECB, BoC Rate Decisions

With non-farm payrolls data now behind us, the focus for the Greenback arguably turns to external economic event risk. That is because the domestic calendar is fairly light and quiet. Dallas Fed President Robert Kaplan will be speaking later this week. Traders will likely be tuning in to see what he has to say about the labor market and what that could mean for policy going forward.

In the coming week, the Reserve Bank of Australia (RBA), European Central Bank (ECB) and Bank of Canada (BoC) will be releasing their latest monetary policy announcements. Recent economic developments out of Australia, the