RAND ANALYSIS

ZAR FUNDAMENTAL BACKDROP

The morning started strong for the South African rand[2] against the U.S. dollar[3] as local IHS PMI data printed above 50 (see data below) for the first time since June which suggests an expansion in business activity.

Source: DailyFX economic calendar[4]

Unfortunately, for rand bulls this is where the positive news ends (for now at least). Focus is firmly on the United States and the issues surrounding rampant inflation[5] coupled with slow economic growth. The ‘stagflation’ term has been thrown around lately and could hurt the rand should the trend continue.

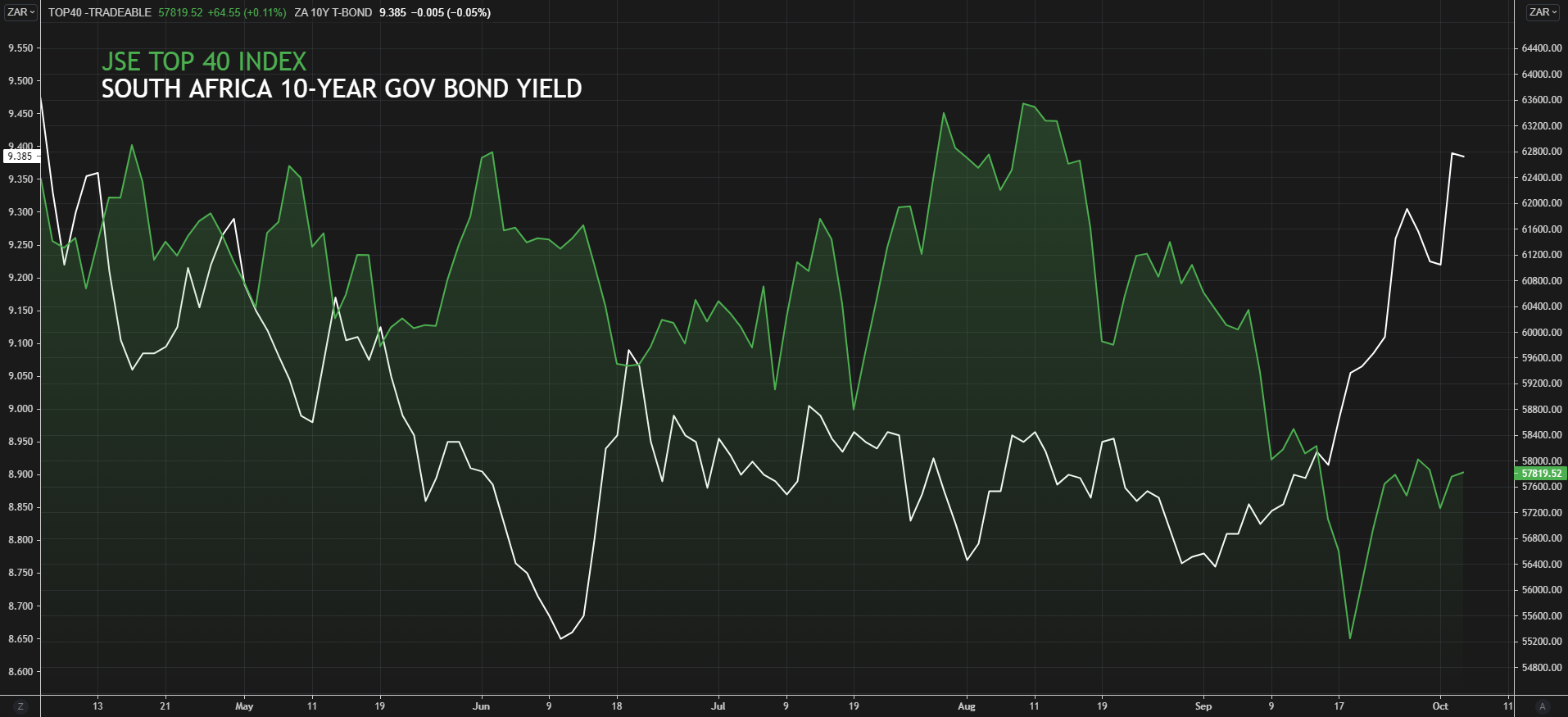

U.S./China tensions have also been escalating along with concerns around Evergrande. Both influencing factors pose negative implications for the ZAR and are evident through the local equity and bond markets respectively – see chart below. The chart reflects the slump in the JSE Top 40 index while government bonds outflows have risen exhibited by rising yields (declining bond prices) . Less demand for the ZAR thus spilled over to the FX market resulting in rand depreciation, while upcoming local elections will add in extra volatility during Q4 2021.

JSE TOP 40 VS SA 10-YEAR GOVERNMENT BOND YIELD

SOUTH AFRICAN RESERVE BANK MISSING A TRICK?

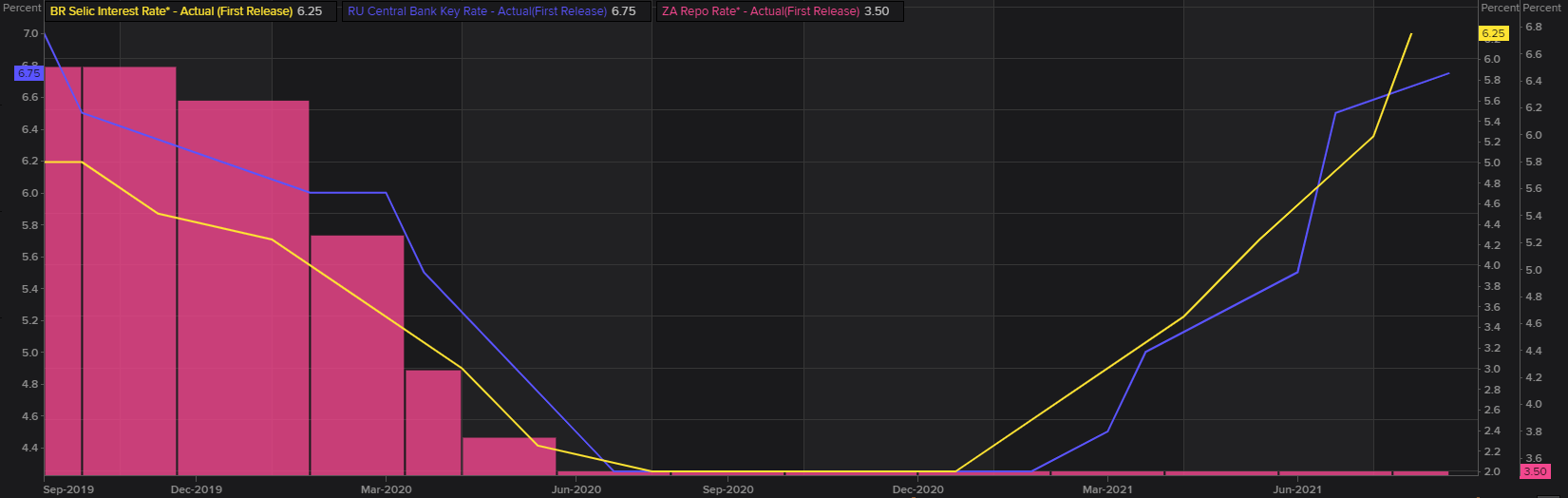

Emerging Market (EM)[6] peers such as Russia and Brazil have already begun tightening (see chart below) while the SARB still remains accommodative. Of course lower rates suit businesses and individuals looking to borrow capital but there are potential drawbacks in this current economic environment.

INTEREST RATES: SOUTH AFRICA (PINK), RUSSIA (BLUE) AND BRAZIL (YELLOW)

Source: Refinitiv

The