British Pound Weekly Fundamental Analysis: Mixed

- Retail sales continue downward run as September data worse than expected

- Markit PMIs remain strong as inflation indicators soar but consumers turn more pessimistic

- Rates markets pricing in November hike and new daily Covid cases surpass 50k - highest in Europe

There are a number of drivers and potential drawbacks to the Pound[1] Sterling as we approach the November 4 rate decision which justifies a more cautious approach to GBP based setups.

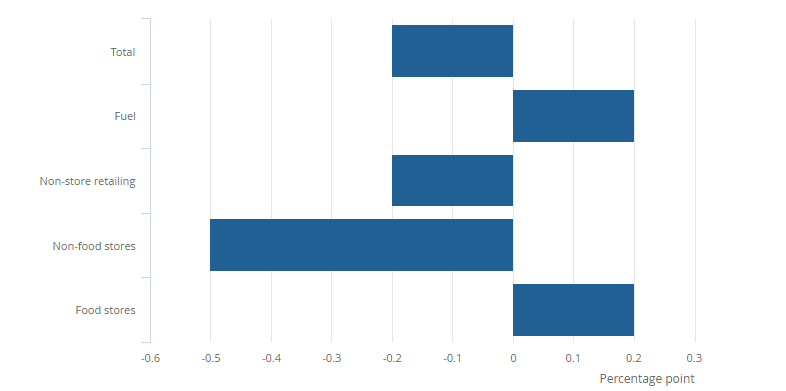

Household Goods Stores Drag the Retail Sector Lower

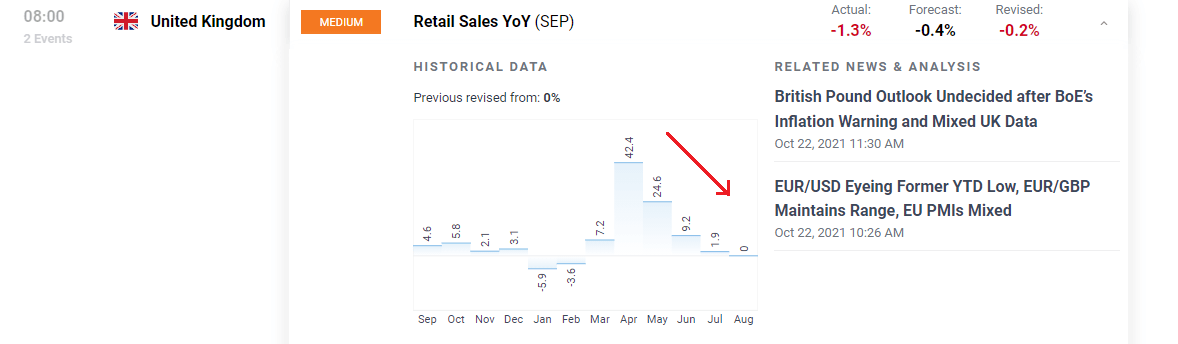

UK retail sales for September, compared to September last year, declined significantly from expectations. The 1.3% contraction, spearheaded by lacking figures from the ‘non-food retail stores’ weighed heavy on the wider sector as only a 0.4% contraction was forecasted.

For all market-moving data releases and events see the DailyFX Economic Calendar[2]

The current series of declining retail data is described by the Office for National Statistics (ONS) as, “the longest period of consecutive monthly falls in history of this series (which began in February 1996)”

Source: Office for National Statistics (ONS)

PMI Sentiment Diverges from Consumer Sentiment

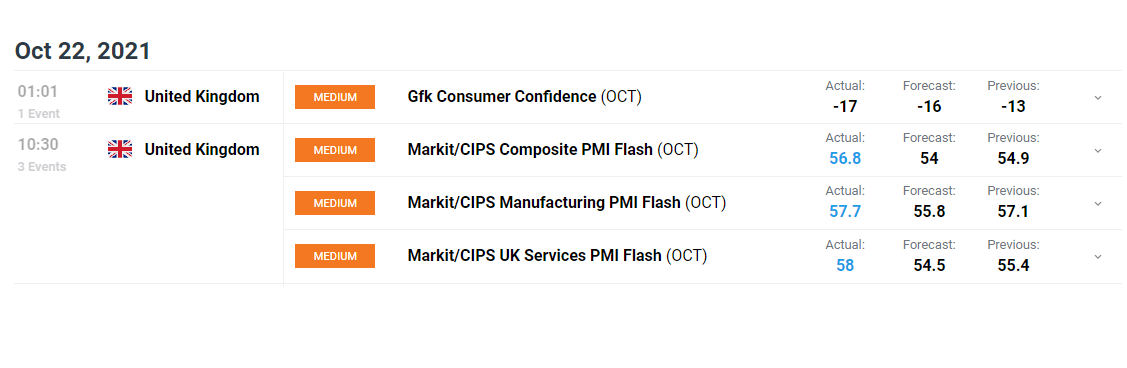

Flash (preliminary) Markit PMI data beat expectations in both the manufacturing and services sectors. Both readings came in above 50 meaning purchasing managers anticipate an expansion in both sectors.

Consumer confidence readings however, tell a different story as the reading posted (-17). The survey is forward looking and asks a sample group of 2000 consumers to gauge their personal financial situation and the overall economic environment for the next 12 months.

Inflation Expectations

One factor, identified by the Gfk survey, adding to consumer pessimism is the current and future level of prices. Global supply chain challenges and increasing demand has lead to sustained elevated fuel and gas prices which