BRENT CRUDE OIL (LCOc1) TALKING POINTS

- OPEC+ increases output target.

- Attention shifts to key Chinese and U.S. data.

BRENT CRUDE OIL FUNDAMENTAL FORECAST: MIXED

Brent crude oil[1] finished the week off strong post-NFP[2] despite a stronger U.S. dollar[3]. We saw OPEC+ agreeing to an increase of approximately 648Mbbls/d for July and August respectively which is a marked increase from the previously agreed upon 432Mbbls/d. Interestingly, the increase in supply included Russia despite reports of a potential exclusion due to sanctions on Russian oil[4].

Learn more about Crude Oil Trading Strategies and Tips in our newly revamped Commodities Module![5]

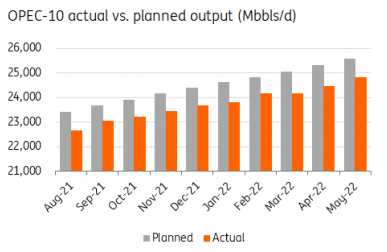

Typically, an increase in supply of this magnitude should ease crude oil prices[6] but with OPEC+ member nations currently struggling with supply targets at a much reduced volume, the 648Mbbls/d looks like a stretch for many contributing nations. The graphic below from ING illustrates the shortfall leading up to the revised supply target. I do not see this trend changing over the next two months which should keep crude oil prices elevated.

Source: ING

U.S. inventories as reported by the Energy Information Administration (EIA) supplemented oil bulls after significant drawbacks in stockpiles allowing for a breach of the $115/barrel resistance level.

Another key factor to crude oil prices stems from the demand-side, and in particular the Chinese economy. Being the largest consumer of crude oil, the hindrance of COVID-19 has negatively impacted demand forecasts and consequently muted crude oil price increases.

ECONOMIC CALENDAR

Looking ahead to next week, the China theme kicks off the trading week with PMI data which has been on the decline since December 2021. Another print lower could weigh negatively on crude oil.

From the dollar perspective (historically