Talking Points:

- March Fed rate hike odds remain at 100%, but odds for four hikes in 2018 are still below 40%.

- The DXY[1] Index will have a difficult time breaking through 91.01, the key level eyed before a bottom can be called.

- See the full DailyFX Webinar Calendar[2] for upcoming strategy sessions.

Looking for longer-term forecasts on the US Dollar? Check out the DailyFX Trading Guides[3].

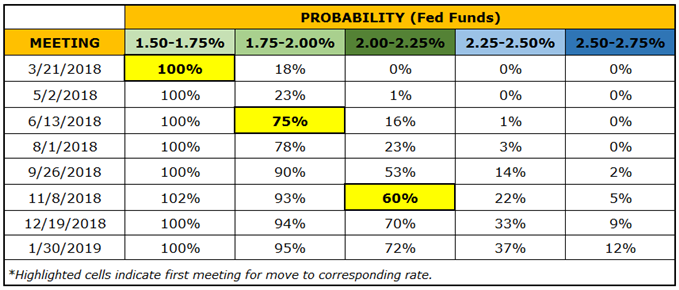

Ahead of the March FOMC[4] meeting concluding later today, Fed funds futures are pricing in a 100% chance of a rate hike – just as they have since the start of 2018. As has been the case when front month odds are at 100%, the direction of the US Dollar is not contingent on the Fed raising rates but rather what expectations are set for the path of rate hikes down the line.

Currently, rates markets are pricing in additional 25-bps hikes in June and November, with a 33% chance for a fourth rate hike in 2018 by December.

Table 1: Fed Rate Hike Expections (March 21, 2018)

Accordingly, the biggest source of volatility for the US Dollar will come from the updated Summary of Economic projections, the first released under the purview of newly-minted Fed Chair Jerome Powell. At his testimonies to Congress in February, Chair Powell suggested that recent developments in the US economy, including a more stimulative fiscal policy vis-à-vis the Trump tax cuts, will result in both growth and inflation expectations being upgraded.

While upgrades to the forecasts should, in theory, be positive for the US Dollar, there has been a discernible disconnect between the US Treasury bond market and FX markets – higher yields have not Fed into a stronger currency. Interest rate differentials, historically the main influence over FX, have proven unimportant. We suspect then that the relationship between US equity markets and FX markets will prove to be the key driver.

Price Chart 1: DXY Index Daily Timeframe (August 2017 to March 2018)

It would stand to reason that given the inverse relationship between the S&P 500[5], for example, and the US Dollar since the start of 2018, that fears of a faster Fed tightening cycle leading to a selloff in stocks would prove to be the most fertile grounds for US Dollar gains.

With a backdrop as such, EUR/USD[6] appears set to stay within the key reversal range carved out between 1.2155 and 1.2456; USD/JPY[7] should stay within its downtrend from January 8 below the daily 21-EMA; and GBP/USD's recent bullish pennant breakout should stay intact.

Likewise, it would appear that the DXY Index may not find the FOMC meeting as the catalyst it